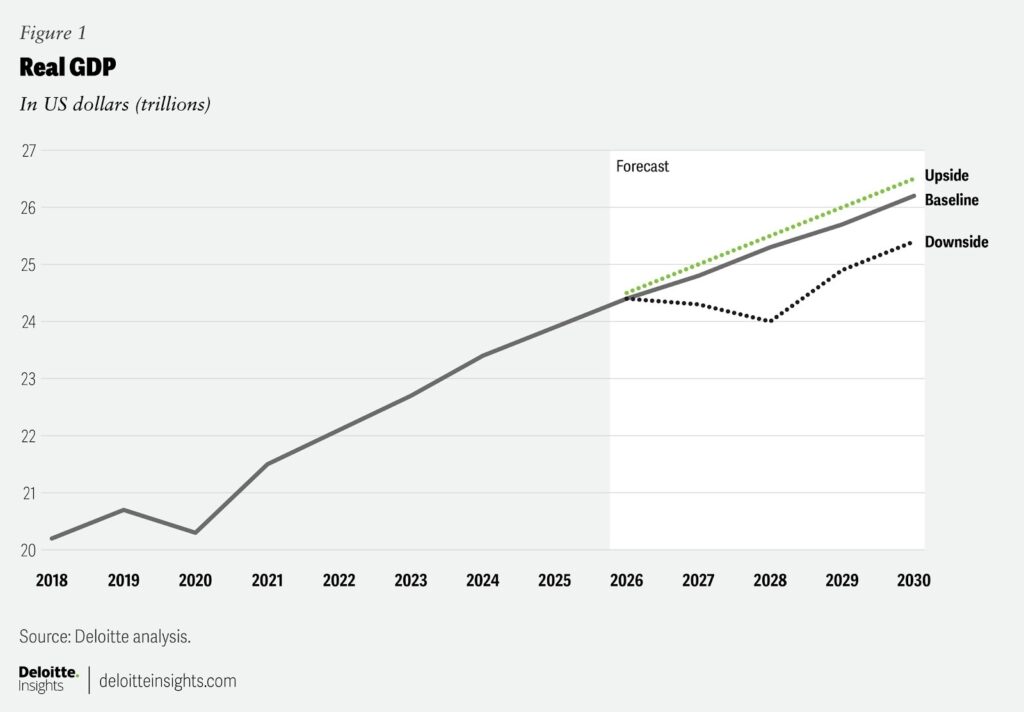

The US economy growth rate in 2026 is the centre stage for economists, businesses, investors, and everyday Americans as we go through April 2026. With Q4 2025 real GDP growth at a lackluster 0.7% (which followed a stronger 4.4% in Q3 2025), and full-year 2025 settled at around 2.1–2.2%, focus unambiguously turns to what’s next.

Forecasts for the US economy growth rate in 2026 tend to concentrate in the 2.0–2.5% zone among leading guides, indicating a resilient but decelerating expansion. This pace is a bit above potential growth over the long haul (estimated at around 1.7–1.8%) on account of ongoing AI-led investment, fiscal tailwinds from 2025 legislation, and a bounce from late-2025 disruptions such as the government shutdown. But tariffs, migrant labor shortage,s and high energy prices linked to tensions in the Middle East, along with a patchy pattern of consumer spending, paint a more complicated portrait.

US Economic Forecast Q1 2026 | Deloitte Insights

This in-depth guide explores the latest data, consensus forecasts, key drivers, sector impacts, risks, and implications of the US economy growth rate in 2026. Whether you’re tracking GDP trends, planning investments, or assessing job security, here’s everything you need to know about the US economy growth rate in 2026.

Recent Performance: Setting the Stage for 2026

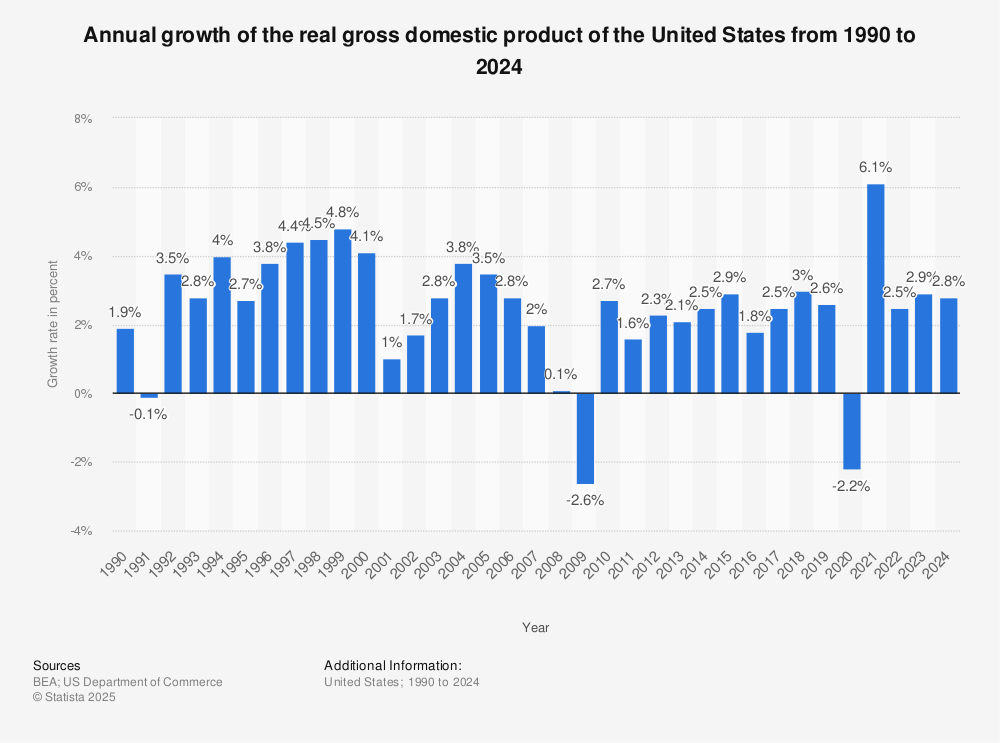

There is a need to look back at 2025 in order to gauge the US economy growth rate in 2026. Real GDP was up about 2.1–2.2% for the year, compared with 2.8% in 2024. Consumer spending and private investment were the main contributors, but Q4 2025 underperformed with just 0.7% annualized growth—the slowest since Q1 2025. That weakness was due to downward revisions in exports, consumer spending, government outlays, and investment, some of which were offset by lower imports.

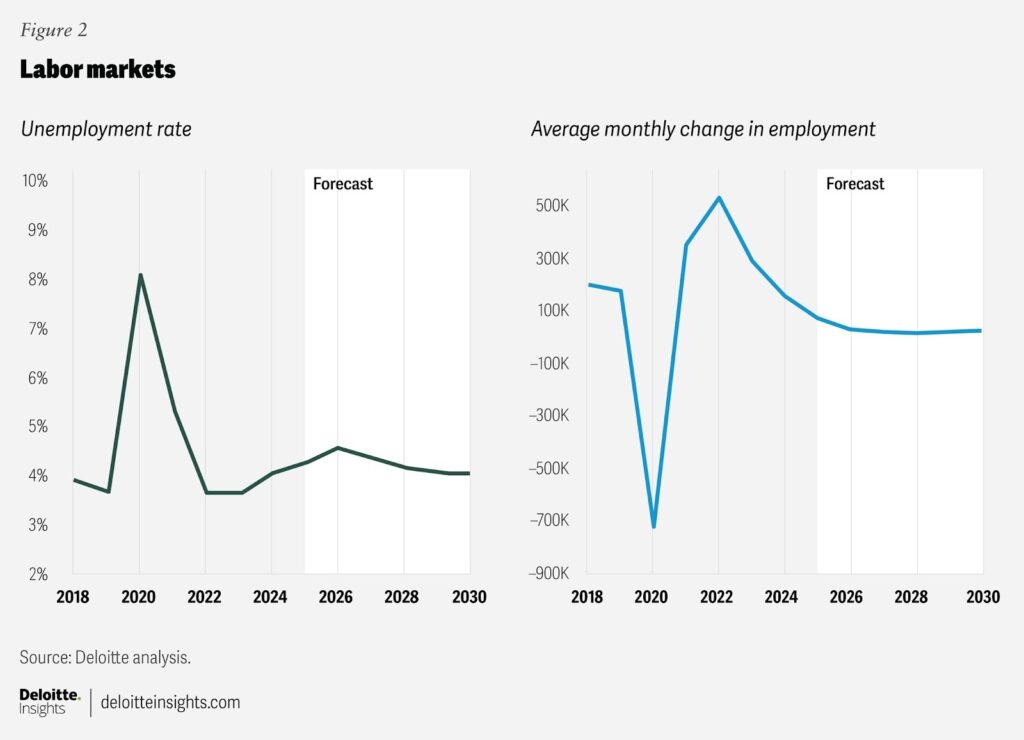

And the labor market has also cooled. Monthly job growth had slowed sharply amid drastically curtailed immigration flows, and it found the unemployment rate settling near 4.4–4.5% as of early 2026. Productivity stayed robust, however, propelled by AI adoption that is enabling output to be sustained without any breakneck hiring.

Historically, the post-pandemic bounce is more clear: first with contraction and then a strong rebound in 2020, the US has avoided recession over the subsequent two-year period, even against policy changes — including extensive tariffs that raised average rates to about 17%.

Real GDP growth rate U.S. 2024| Statista

These factors—fiscal stimulus fading in places, trade policy effects materializing, and technological tailwinds—shape the baseline for the US economy growth rate in 2026.

Consensus Forecasts for the US Economy Growth Rate 2026

Forecasters generally agree the US economy growth rate in 2026 will land between 1.8% and 2.8%, with most clustering around 2.0–2.4%. Here’s a breakdown of key projections as of early 2026:

- Congressional Budget Office (CBO): 2.2% real GDP growth in 2026, accelerating from 2025 due to the 2025 reconciliation act (boosting consumption and investment) and rebound from the late-2025 shutdown. Growth then moderates to 1.8% in 2027 as fiscal boosts fade.

- International Monetary Fund (IMF): 2.4–2.5% (Q4/Q4 or annual basis), with growth accelerating modestly as tariff effects wane and oil prices ease. Unemployment stays near 4%, and core PCE inflation returns toward 2% by mid-2027.

- Goldman Sachs: More optimistic at 2.8% full-year (2.5% Q4/Q4), citing fading tariff impacts, tax cuts from the One Big Beautiful Bill Act, and strong business/personal spending. They see US growth outperforming consensus.

- Deloitte: Healthy 2.2% growth, driven by stronger 2025 carryover effects and AI-supported business investment (expected +4%). Consumer spending moderates to 2.1%.

- Vanguard: 2.3% (recently downgraded 0.2 points), reflecting firmer energy prices and tariff pass-through, offset by resilient household demand and AI capex.

- Other consensus views (Blue Chip, Philadelphia Fed Survey, S&P Global): Around 1.8–2.0%, with professional forecasters seeing 1.9% median. Risks are balanced near-term but tilted by energy prices.

On balance, real US gross domestic product in 2026 is forecast to modestly exceed potential output in the first half of the year and then return to norms. GDPNow estimates for Q1 2026 are around the same, and still insist on a soft start before reaccelerating.

These forecasts include existing laws and are based on no major new shocks. Upside scenarios (more powerful AI, a massive demand surge) could boost growth above 3 percent; downside risks (tariffs that don’t go away, surging oil prices) could drag it below 1.5 percent.

Key Drivers Shaping the US Economy Growth Rate 2026

Several interconnected forces will determine whether the US economy’s growth rate in 2026 hits the higher or lower end of forecasts.

1. Fiscal Policy and the 2025 Reconciliation Act

All of this is codified in the One Big Beautiful Bill Act (and various other 2025 on-the-table measures) to provide a near-term shot in the arm through smashed down individual taxes (increasing disposable income) and full expensing for select capital expenditures. That moves activity from late 2025 into early 2026, underpinning consumer spending and private investment. The effects are also transitory beyond mid-year, and higher deficits (estimated at around 6% of GDP) raise questions about long-term debt sustainability.

2. AI-Driven Business Investment

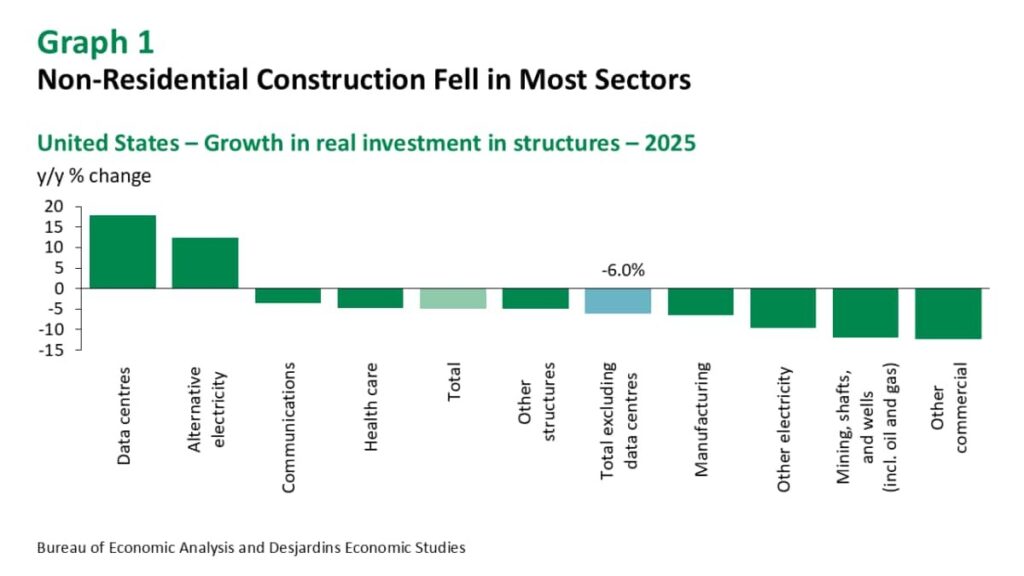

AI capex remains a standout pillar. Hyperscalers plan hundreds of billions in data centers and related infrastructure, driving non-residential investment growth. This offsets weakness elsewhere and boosts productivity, potentially adding 0.5–1 percentage point to GDP. Sectors like tech and communications see outsized gains.

AI Drove the Majority of US Business Investment in 2025 – Desjardins

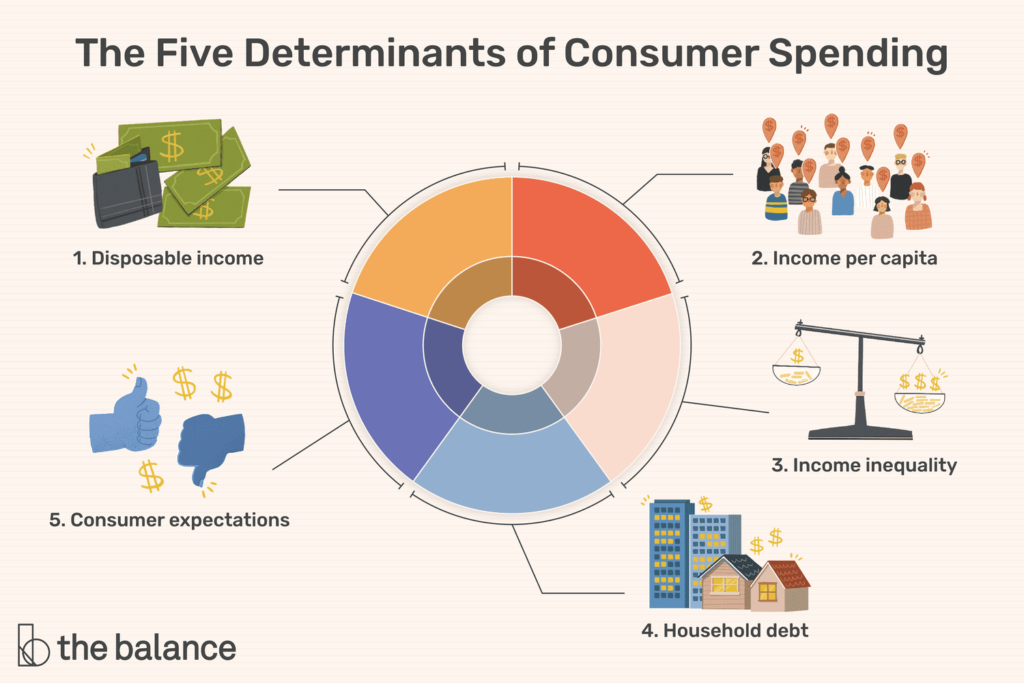

3. Consumer Spending and Household Resilience

Consumer spending (≈70% of GDP) is expected to moderate to ~2.1% growth. Strong real wages, asset prices (stocks, homes), and tax refunds help, but higher energy prices, tariff-induced inflation, and labor market cooling weigh on sentiment. The “new consumer” is more fragmented, with disparities in spending power.

Consumer Spending and Its Impact on the Economy

4. Trade Policy, Tariffs, and Immigration

Tariffs (implemented in 2025) act as a headwind, raising input costs and pressuring consumption/investment. Effects are partially absorbed via pre-stocking, but full pass-through could slow growth by 0.2–0.5 points. Reduced immigration slows labor force growth to ~0.3–0.4% annually, constraining potential output but keeping unemployment stable near 4–4.5%.

5. Monetary Policy and the Federal Reserve

The Fed is expected to deliver limited easing (perhaps one cut) if inflation moderates. Higher energy prices from Iran-related tensions create upside inflation risks, potentially keeping rates steady longer. Neutral policy supports moderate growth without overheating.

6. Energy Prices and Geopolitics

The conflict in Iran has spiked oil prices, weighing on consumption but benefiting the energy sector (the US as a net exporter). Models suggest a modest net drag on GDP unless the conflict escalates.

7. Productivity and Potential Output

AI and technology investments sustain strong productivity, helping the economy grow faster than labor-force constraints would otherwise allow. Long-term potential growth remains ~1.7–1.8% due to demographics.

US Economic Forecast Q1 2026 | Deloitte Insights

Sector-by-Sector Outlook for 2026

- Technology & AI: Strongest performer. Data centers and AI infrastructure drive construction and equipment investment (up double-digits in some areas). Job creation in AI-related fields is concentrated in states like California, Texas, and Virginia.

- Manufacturing & Trade-Sensitive Industries: Mixed. Tariffs provide some protection but raise costs; recovery in industrial production may stall if input shortages persist.

- Energy: Boosted by higher prices and domestic production; investment in alternative electricity and oil/gas remains solid.

- Consumer Services & Retail: Moderate growth. Health care continues structural expansion; discretionary spending faces headwinds from prices and uncertainty.

- Government & Construction: Rebound from 2025 shutdown supports early-year activity, but non-residential structures (excluding data centers) face declines.

Risks and Uncertainties for the US Economy Growth Rate 2026

Downside Risks:

- Persistent or escalating tariffs/geopolitical tensions → higher inflation and slower consumption.

- Labor supply constraints → weaker job growth (potentially near zero by 2027) and stalled output.

- Recession probability: Low (20% per Goldman) but not zero if energy shocks intensify.

Upside Risks:

- Faster AI productivity gains or stronger fiscal stimulus → growth exceeding 3%.

- Easing inflation, allowing more Fed cuts → supportive financial conditions.

The balance tilts modestly to the downside in some views, but adaptability and private-sector strength provide buffers.

Global Context and Comparisons

The US is expected to do better than most advanced economies (world growth 3.3% by 2026). The outlook for Europe is slower growth (1.4–1.8%) as energy and trade weigh; emerging markets have a wide range of possibilities. Strong domestic demand and tech leadership boost the US economy growth rate narrative for 2026e.

Implications for Businesses, Investors, and Individuals

- Businesses: Prioritize AI investment, supply-chain resilience, and tariff navigation. Capex in tech and energy offers opportunities.

- Investors: Moderate growth supports equities (especially AI/tech), but watch inflation and rates. Diversification remains key.

- Individuals: Job market stays healthy but slower hiring; focus on skills in high-demand sectors. Higher prices may pressure budgets, offset by wage growth and tax relief.

Conclusion: Steady but Watchful Path for the US Economy Growth Rate 2026

Bottom line: Pacing the US economy at 2026’s solid long-run growth rate of 2.0–2.5%—resilient but not supernova—outfitted in AI and powered by fiscal support and consumer fundamentals tempered by policy and external headwinds. Watch for updates as April 2026 data comes in, including Q1 GDP releases, Fed decisions, energy markets, and tariff adjustments.

The American economy has been anything but rigid. Thanks to productivity gains from technology and sound policy, the growth rate of the US economy in 2026 can ensure expansion and opportunity continue. Keep an eye out, as minor adjustments to these drivers could lead you to a significantly different path.