The question at the start of April 2026 is: Is the US economy collapsing? News headlines are dominated by a sharp deceleration in Q4 2025 GDP (downwardly revised to only +0.7% annualized growth), surprise job losses of 92,000 in February 2026, and tortured stock markets during the Iran conflict and policy pivots. But official data, and forecasts from Deloitte, the Congressional Budget Office (CBO), and the Federal Reserve tell a different story: The US economy is not crashing. It is seeing visible moderation — a slowdown after years of pandemic-era robustness — but it’s still in positive growth territory, with low inflation and a labor market that, yes, is cooling but isn’t on the verge of collapse.

This is a deep dive covering all the major indicators by way of the most recent releases from the Bureau of Economic Analysis (BEA), Bureau of Labor Statistics (BLS), and private-sector outlooks. We’ll tackle GDP trends, employment data, inflation dynamics, stock market performance, recession signals,s and key risks (tariffs and immigration policy to geopolitics) — along with the bright spots like AI-driven investment that remain a support for expansion. By the end, you’ll know if is the us economy crashing — and what it means for businesses, investors, and households in practical terms.

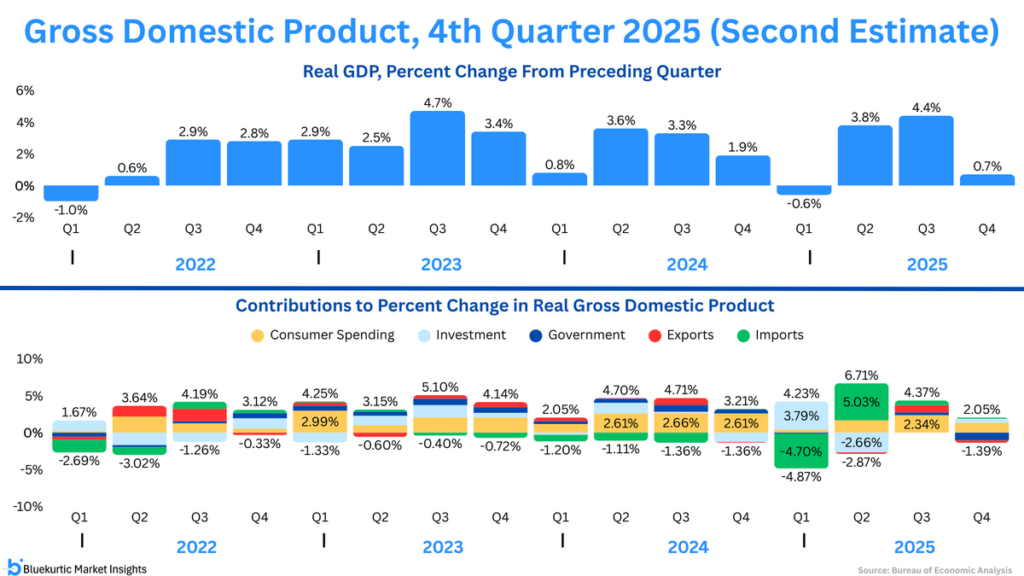

US real GDP grew 0.7% (annualized) in Q4 2025, sharply slowing from 4.4% in Q3, per the BEA second estimate. Growth was driven by consumer spending and investment, while government spending and

Figure 1: Real GDP Growth by Quarter (2022–2025, Second Estimate for Q4 2025) – Growth slowed dramatically to 0.7% in Q4 2025 from 4.4% in Q3, partly due to a government shutdown, but consumer spending and investment provided some support.

Defining an Economic “Crash” vs. a Slowdown

To answer whether the US economy is crashing, we must first clarify the term. A true economic crash involves:

- Sustained negative GDP growth (two or more quarters of contraction, qualifying as a recession per NBER standards).

- Unemployment is surging well above 6–7%, with widespread layoffs.

- A stock market decline of 20%+ from recent highs (a bear market escalating into crash territory).

- Credit market freezes, bank stress, or consumer panic lead to a vicious cycle.

In contrast, a slowdown would show decelerating but still positive growth, mild labor market softening, and stable or moderating inflation. On April 2, 202,6 the US economy looks like the latter. Q4 2025 real GDP great w a revised 0.7% annualized rate—not so impressive compared to both the advance estimate of 1.4% and Q3’s 4.4%—but full-year growth for 2025 was still an admirable 2.2%.

Expectations for 2026 remain in expansion territory at about 2.0–2.3%, once again supported by the stronger base effects from late-2025 and business investment. It is not the 2008 collapse or the 2020 pandemic shock. Is the US economy crashing? The data says no, but risks call for vigilance.

Economy Nearly Stalls in Q4 2025, but a Government Shutdown Shares the Blame

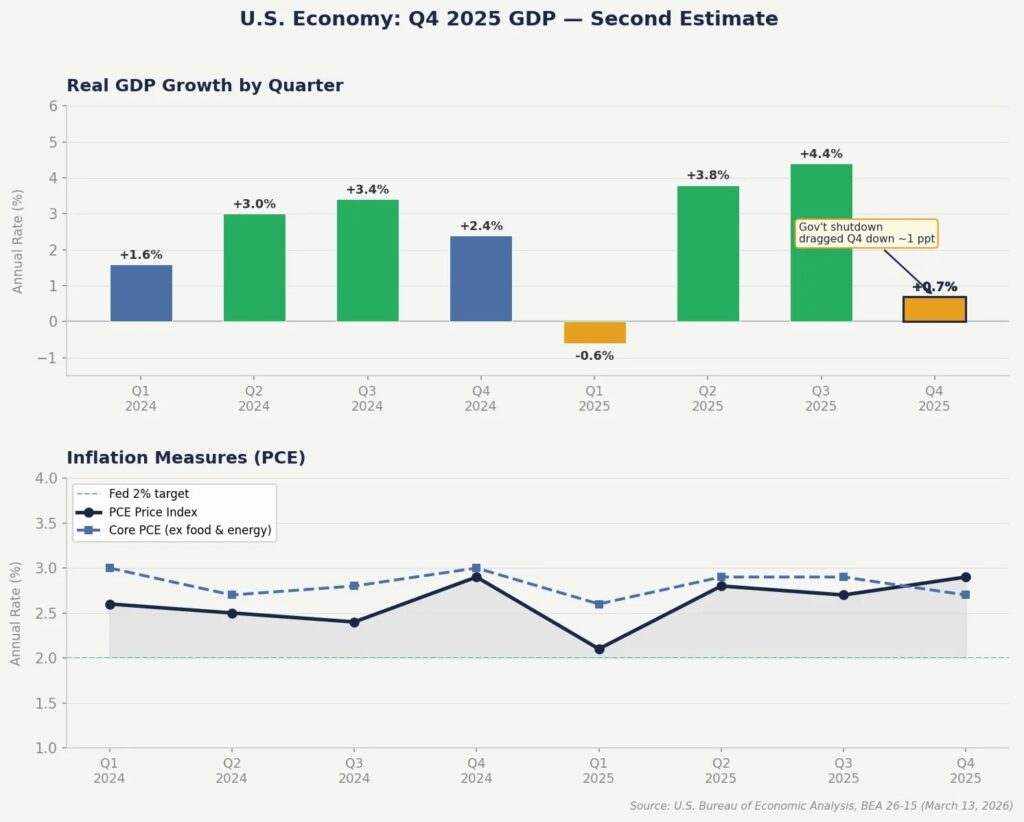

Figure 2: US Real GDP Growth by Quarter with Q4 2025 Highlight – The orange bar shows the sharp deceleration in Q4 2025 to +0.7%, with a note on the government shutdown’s drag of about 1 percentage point.

Latest GDP Data: Positive but Moderating Growth

The BEA’s second stamp on Q4 2025 corroborated weakness: real GDP rose at only 0.7% annualized, down an eighth point from the advance estimate. Downward revisions affected exports, consumer spending, government outlays, and fixed investment. \n• A 43-day government shutdown late in 2025 meaningfully dragged (estimated drag of ~1point)

Still, it appears underlying private-sector demand was stronger than feared. Consumer spending and business investment were bright spots, offsetting disappointing government and export numbers. Q4 full-year 2025 GDP growth was 2.2% compared to 2.8% in 2024, but still solid.

For 2026, the outlook remains constructive:

- Deloitte projects 2.2% real GDP growth, driven by business investment (expected +4%) despite softer consumer spending (around 2.1%). Stronger 2025 data provides a mathematical lift to 2026 figures.

- The Fed and CBO see similar modest expansion, with potential upside from AI and policy incentives in the 2025 reconciliation act.

- Atlanta Fed GDPNow nowcasts for early 2026 have hovered in the 1.8–2.2% range.

Key supports include AI-fueled capital spending and productivity gains. Headwinds—tariffs, reduced immigration impacting labor supply, and energy volatility from the Iran conflict—could temper this, but not enough to trigger contraction. Is the US economy crashing? GDP data firmly indicates a slowdown, not a crash.

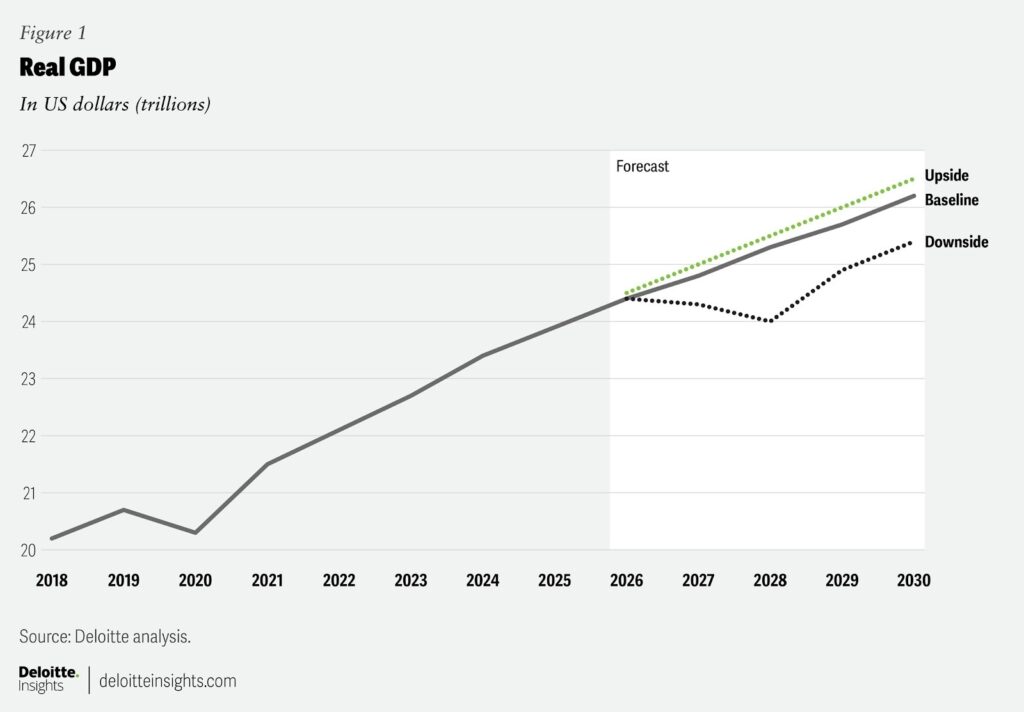

US Economic Forecast Q1 2026 | Deloitte Insights

Figure 3: Deloitte Real GDP Forecast (2018–2030) – Baseline scenario shows continued expansion through 2026 and beyond, with upside potential from policy and technology.

Labor Market: Cooling into a “Low-Hire, Low-Fire” Equilibrium

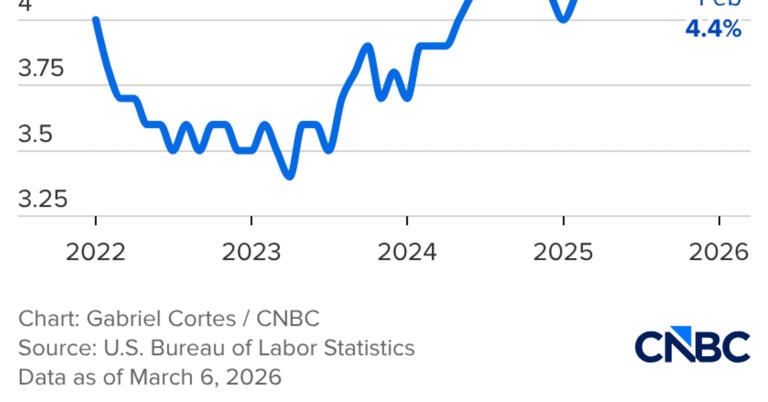

February 2026 BLS data delivered a surprise: nonfarm payroll employment edged down by 92,000—the first notable decline in years—while the unemployment rate ticked up to 4.4% (from 4.3% in January).

US payrolls unexpectedly fell by 92,000 in February; the unemployment rate rose to 4.4%

Figure 4: US Unemployment Rate Trend (2022–Early 2026) – The rate rose modestly to 4.4% in February 2026, remaining historically low despite slowing job growth.

This softness stems partly from sharply reduced immigration, which has lowered the “breakeven” job growth needed to hold unemployment steady—now near zero or even negative in some models. Health care saw losses due to strike activity, and broader revisions to population estimates (reflecting lower net international migration) adjusted labor force figures downward.

Yet context matters:

- Unemployment at 4.4% is still near historic lows (pre-pandemic averages were higher).

- Initial jobless claims remain contained, signaling limited,broad-based layoffs.

- Forecasters expect the rate to peak around 4.5–4.7% in 2026 before stabilizing.

The labor market has shifted to a “low-hire, low-fire” state. While this feels concerning after years of rapid job gains, it does not indicate collapse. Is the US economy crashing? The jobs data points to cooling, not crisis—especially with prime-age dynamics and policy-driven labor supply changes in play.

Inflation: Steady and Near Target, But Watch Energy Risks

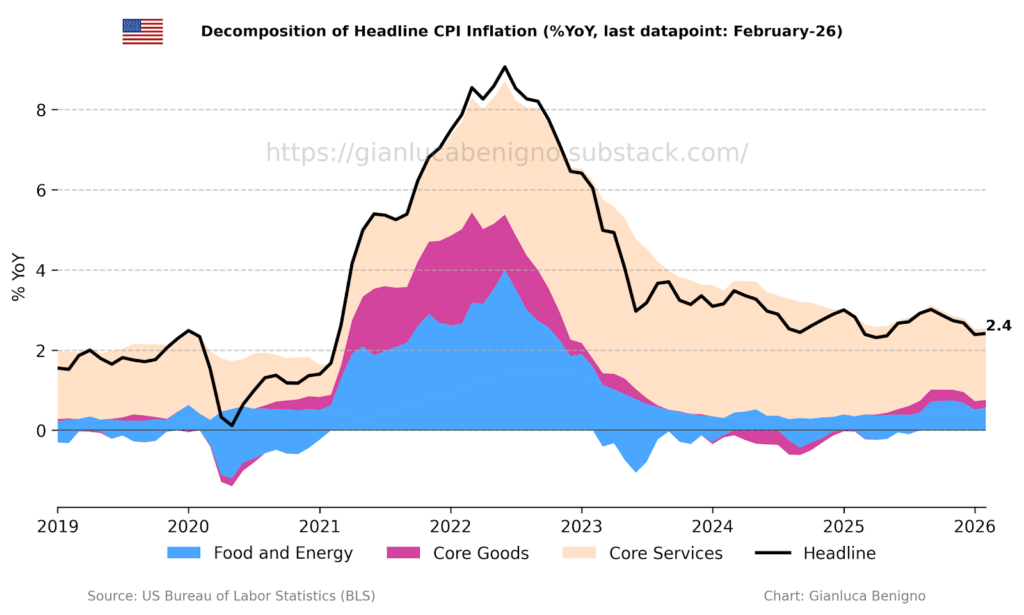

Headline CPI inflation held at 2.4% year-over-year in February 2026—the lowest since May 2025. Core CPI (excluding food and energy) was 2.5%. Food rose 3.1%, energy edged up 0.5%, while shelter and goods pressures continued to ease.

Figure 5: Comparison of Inflation Measures (2022–February 2026) – Headline CPI (blue) and core CPI (orange) have moderated significantly from 2022 peaks, now hovering near 2.4–2.5%.

The monthly CPI rose 0.3% in February. Risks for the rest of 2026 include:

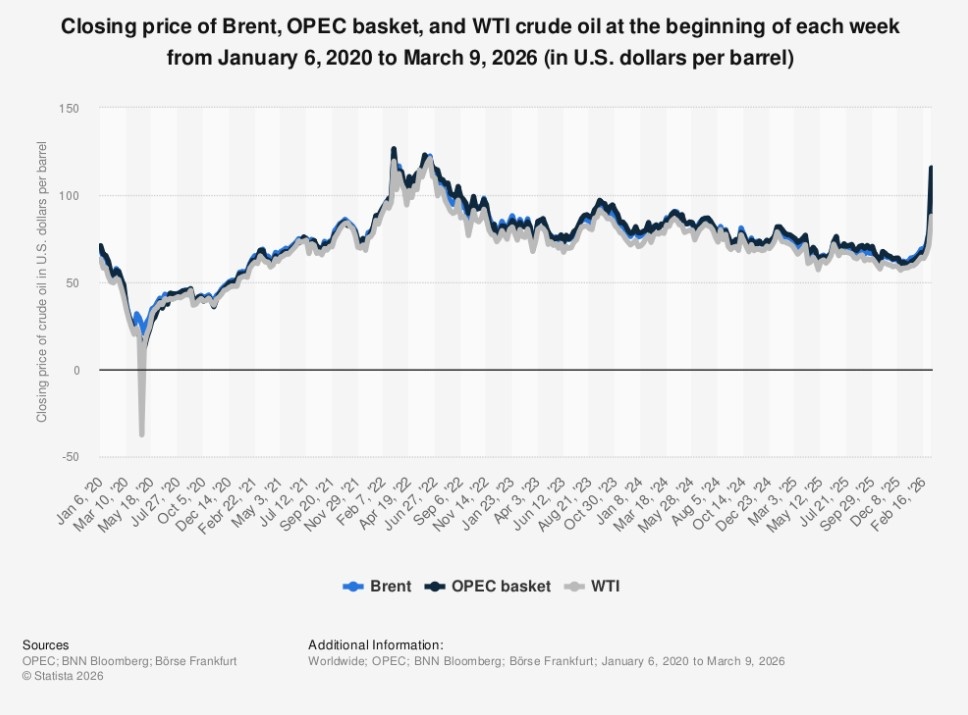

- Prolonged Iran-related oil shocks (prices briefly spiked above $100–120/barrel).

- Tariff impacts on imported goods.

- Fed’s preferred PCE measure is projected aat round 2.7% for the year.

Inflation is not spiraling out of control or reverting to 1970s levels. With the Fed having cut rates in late 2025, policymakers retain flexibility. Is the US economy crashing? Tame price pressures argue strongly against it.

US February-26 CPI Inflation Report – by Gianluca Benigno

Figure 6: Decomposition of Headline CPI Inflation (2019–February 2026) – The black line shows the decline to 2.4%, with contributions from food/energy (blue), core goods (pink), and core services (beige).

Stock Market: Volatile Start to 2026, But No Full Crash

The S&P 500 entered 2026 at record highs but faced volatility, ending Q1 down around 4.6% amid Iran conflict worries, energy spikes, and growth concerns. Broader indices (Dow, Nasdaq) saw similar or steeper pullbacks, briefly testing key moving averages.

The Pyramid of S&P 500 Returns: 152 Years of Market Performance

Figure 7: 152 Years of S&P 500 Annual Returns – Historical context shows 2026 projections (around +12% in some optimistic scenarios) fit within normal variability, though downside risks exist.

Analysts still forecast positive returns for 2026 (e.g., ~10–12% in base cases), supported by corporate earnings growth and AI tailwinds. Valuations remain elevated, raising correction risks, but a 20%+ crash has not materialized. Is the US economy crashing? Markets are nervous and volatile—not in freefall.

Recession Signals: Elevated Odds, But Not Imminent

Polymarket and models place the probability of a recession by the end of 2026 at ~30–34%. The Conference Board’s Leading Economic Index (LEI) has flashed warnings, with several components (yield curve, manufacturing ISM, consumer confidence) in cautionary territory.

Figure 8: Historical US Recession Probability (Conference Board Model Example) – Probabilities spike before past downturns; current readings are elevated but below crisis levels.

Seven of twelve key indicators are in “warning” mode per some analyses, yet near-term models (Fed, private forecasters) see lower immediate risk (~25–30%). The economy has weathered 2025’s shutdown and policy shifts better than many expected. Is the US economy crashing? Recession odds are higher than average, but consensus forecasts point to expansion.

Major Risks That Could Escalate the Slowdown

Several factors could tip moderation into something worse:

- Geopolitics and Energy: The Iran conflict has driven oil volatility; prolonged disruption could push inflation higher and growth lower.

- Trade and Tariffs: Policy uncertainty and tariffs may slow growth and raise costs, particularly for goods.

- Immigration and Labor Supply: Reduced inflows have already reshaped job dynamics; further tightening could constrain growth.

- Fiscal and Debt Pressures: Deficits remain high; CBO projects challenges, though near-term stimulus effects provide some buffer.

- Consumer Affordability: Despite headline resilience, lower/middle-income households face pressures from housing, food, and subsidy changes.

These risks are real and could compound if external shocks intensify. However, they have not yet produced the broad contraction defining a crash.

Bright Spots Supporting Resilience

- AI and Productivity Boom: Heavy investment in generative AI and related technologies acts as a powerful growth engine, boosting business capex.

- Consumer and Private Demand: Spending has held up better than feared; wealth effects from prior market gains provide a buffer.

- Monetary Policy Room: The Fed can adjust rates if needed, following late-2025 cuts.

- Historical Precedent: The US economy has repeatedly defied doomsayers, showing adaptability through policy and innovation cycles.

Sectors like services and technology remain firmer, while manufacturing and housing feel more pressure.

Sectoral and Household Impacts

Soft (weak ISM PMI) manufacturing and goods-producing sectors. Housing is contending with hurdles from rates and affordability. Services hold steadier. Changes to safety-net programs (e.g., SNAP adjustments, ACA subsidies) will most directly impact low- and moderate-income families. But wage growth (albeit slower) and stock/housing wealth are still propping aggregate demand.

Expert Consensus Outlook for 2026

- Deloitte: 2.2% GDP growth, inflation easing, unemployment around 4.5%.

- CBO/Fed: Similar modest expansion with upside from recent legislation.

- Wall Street: Mixed but generally positive on earnings; recession odds 25–40%.

- IMF and Others: Potential for acceleration if global conditions stabilize.

The year is described as “meh” or “make-or-break” by some—positive growth but unspectacular, with policy and external factors decisive.

Final Verdict: Is the US Economy Crashing?

No, the US economy isn’t crashing in April 2026. . It’s slowing: Q4 2025 GDP estimated to be revised down to 0.7%, February job losses at 92k, pushing unemployment rate up to 4.4%, and markets are volatile with declines in Q1. Tariffs, immigration shifts, energy risk,s and policy uncertainty drive recession probabilities ta o 30–34% range. Yet growth continues to be positive, inflation is pinned down around 2.4–2.5%, as are structural supports such as AI investment that should buttress the economy.

Is the US economy crashing is a legitimate question with all the headlines, but the data indicates moderation, not meltdown. Upcoming releases to watch: the March jobs report (April 3), first-quarter GDP (late April), and inflation trends. For individuals and businesses: stay diversified, create buffers, double down on skills in high-productivity sector,s and watch geopolitics closely.

The economy has proved remarkably resilient. If measured policy responses are followed by de-escalation of external shocks, 2026 can still bring steady — if not spectacular — expansion. Things are changing quickly; keep your eye on the data, not the headlines.