Effective cash management is the backbone of sustainable corporate growth in today’s fast-paced world. The business money market is one of the most effective and frequently underutilized tools that a corporation of any size has at its disposal. Regardless of whether you run a startup in Dhaka, are a mid-sized manufacturer, or even a multinational corporation, by learning more about the business money market, you can enhance your liquidity decisions, earn an attractive rate of return on excess cash, and fund short-term needs without the commitments of long-term debt.

The business money market is that part of the financial system concerned with the borrowing and lending of money for short periods—typically, those having maturities of one year or less. It is an important link between cash-rich businesses and those in need of immediate funding.” The business money market looks to liquidity, safety, and efficiency (unlike the capital market,t which is in stocks and long-term bonds).

Industry Brief: By 2026, as global economies continue to hum along on resilient growth with moderating interest rates and persistent AI-driven investments, the business money market now sees record levels of institutional participation. Companies are using it more than ever, not just to park excess funds but also for tactical cash-flow management in an era of sticky inflation and shifting digital finance tools.

This extensive 2,500+ words guide covers the full spectrum of business money market topic — with core definitions and instruments explained, along with real-life usage examples (pros & cons), comparisons to other investment vehicles, and finally (just in case you were wondering) trends for 2026 — so that you can take informed decisions to grow your company.

What Is the Business Money Market?

Never miss a momentum trading strategy – sign up for our free Bullish Dollar newsletter. Features of the business money market:t The business money market is a decentralized over-the-counter (OTC) financial Marketplace where members globally purchase and sell highly liquid short-term debt securities. These span governments, banks, corporations, and institutional investors. The goal here is to even out temporary cash surpluses and deficits while keeping the broader financial system stable.

The commercial money market is defined by key characteristics:

• Maturity: Typical of 1 day to 1 year (most under 270 days to sidestep registration necessities at the SEC for industrial paper).

• Low credit risk — instruments are issued by quality borrowers (governments, blue chip corporations, banks).

• High liquidity: The asset can be turned into cash easily without pricing issues.

• Modest but predictable returns: better than checking accounts, worse than stocks or long bonds.

For corporations, the business money market serves both as a savings vehicle (for investing excess cash) and as a borrowing channel (to raise working capital quickly and cheaply). It saves companies from the higher interest rates and longer approval processes of traditional bank loans while providing a refuge for cash that would otherwise sit idle in low-yield checking accounts.

Unlike the volatile world of stock markets, the business money market is focused on capital preservation and daily accessibility—two qualities that are perfect for treasury departments dealing with payroll, paying suppliers, or seasonal cash flows. Basically, it helps keep the wheels of commerce moving smoothly.

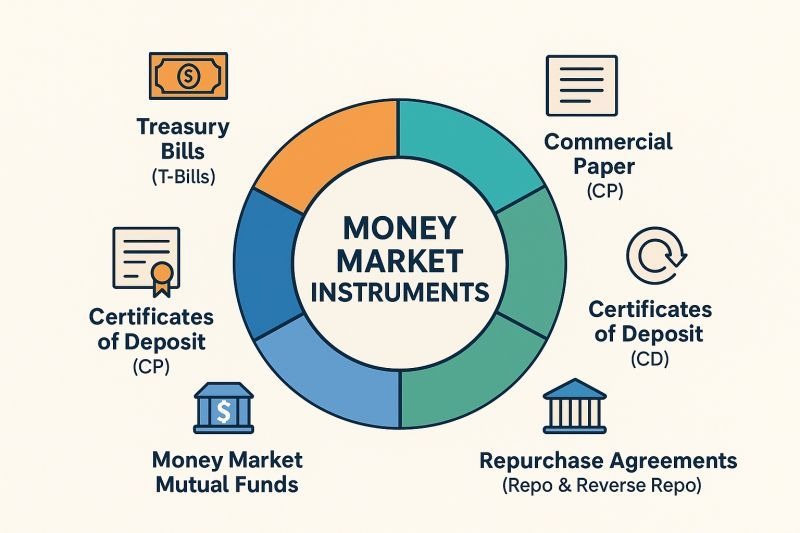

Key Instruments in the Business Money Market

The business money market offers a diverse toolkit of instruments. Each serves specific needs while maintaining the core principles of safety and liquidity. Here are the most important ones businesses rely on daily.

- Treasury Bills (T-Bills) Backed by the government (e.g., U.S. Treasury or respective sovereign agencies), T-bills are zero-coupon instruments sold at a discount and redeemed at par. The maturities range from 4 weeks to 1 year. They are regarded as the safest instrument in the business money market because they have virtually no credit risk. Businesses buy T-bills to safely park large cash reserves while earning a low yield that typically tracks central bank policy rates.

- Commercial Paper (CP) Unsecured promissory notes issued by large, creditworthy corporations to fund short-term needs such as inventory or payroll. Maturities are typically 1–270 days. For issuing companies, CP is usually cheaper than bank loans. For corporate investors, it provides better yields than T-bills with low risk (if the issuer is highly rated). Commercial papers are considered a key business money market strategy,y and multiple Fortune 500 companies utilize commercial paper programs.

- Certificates of Deposit (CDs): A type of time deposit, offered by banks with fixed maturities (generally 1–12 months) and fixed interest rates. Negotiable CDs can be traded in the secondary money market for business. The main reason that businesses like CDs is the FDIC or equivalent insurance (up to a certain limit) and predictable returns. They’re great for companies that want marginally higher yields than savings accounts without losing safety.

- Repurchase Agreements (Repos) – Short-term collateralised loans where one party sells securities (typically government bonds) to another, with the agreement that it will buy them back later at a markup. Overnight repos are common. Banks and corporations rely on repos heavily for managing daily liquidity. In the business money market, repos provide ultra-safe, collateral-backed returns and are a pillar of interbank lending.

- Pooled investment vehicles that invest in the above instruments, such as Money Market Funds (MMFs) / Mutual Funds. They seek a stable $1 NAV and same-day liquidity. Institutional MMFs are super popular among businesses, given that they offer diversified exposure, professional management, and access through brokerage platforms. As of early 2026, global institutional money market fund assets have peaked at around $8 trillion—despite moderating yields—and are converging with the levels typical in most developed countries.

Money Market Instruments & Function: Treasury Bills, CP, CDs, Repos, Call/Notice Money | Rhutuja Belkar posted on the topic | LinkedIn

Bankers’ Acceptances and Call/Notice Money Bankers’ acceptances are short-term drafts guaranteed by banks, often used in international trade. Call money allows borrowing or lending on demand (overnight). These complete the flexible toolkit available in the business money market.Each instrument is chosen based on the company’s cash-flow horizon, risk tolerance, and return objectives—making the business money market highly customizable for businesses.

How Businesses Utilize the Money Market

Companies engage with the business money market in two primary ways: as investors (parking surplus cash) and as borrowers (raising short-term funds).

Cash Management & Investment

A manufacturing company with seasonal sales might place its excess cash from a quarterly operation into money market funds or T-bills instead of leaving it in an interest-bearing checking account earning 0.01 percent. That creates a significant return, yet is on hand for unforeseen expenditures. Treasury teams typically run idle balances nightly to both repos and MMFs for max yield.

Short-Term Borrowing: Rather than tapping expensive revolving credit lines, a retailer preparing for holiday inventory demand can issue commercial paper. This is often less expensive and more efficient. Big companies keep issuing CP programs rated by agencies such as S&P or Moody’s to be easily accessed from the commercial money market.

Example: Big tech businesses with healthy balance sheets tap the business money market to temporarily finance AI infrastructure capex before pursuing longer-term bond issuance. Emerging economy mid-market businesses (Bangladesh included) deploy the local equivalents of T-bills and interbank repos to cover working capital efficiently.

Professional analysis tools and platforms have also integrated real-time business money market data, enabling CFOs to instantly monitor yields and liquidity.

Professional Market Research Images,

Benefits of the Business Money Market

The advantages explain why the business money market remains indispensable:

• Superior Liquidity: Most instruments settle in T+0 or T+1, giving businesses instant access to funds.

• Capital Preservation: Extremely low volatility and high credit quality protect principal.

• Competitive Yields: In 2026, even with declining rates, MMFs and short-term instruments still outperform traditional savings accounts.

• Diversification & Flexibility: Mix instruments to match exact cash needs.

• Cost-Effective Borrowing: Commercial paper and repos often beat bank loan rates for qualified issuers.

• Regulatory Safety Nets: Government backing (T-bills) or insurance (CDs) adds peace of mind.

Businesses report higher operational efficiency and stronger balance sheets when actively using the business money market.

Risks and Mitigation Strategies

No financial tool is risk-free. The main risks in the business money market are:

- Interest Rate Risk — Yields fall when central banks cut rates (a likely scenario in 2026), reducing returns on new investments.

- Credit Risk — Rare but possible if an issuer defaults (mitigated by sticking to AAA-rated or government-backed paper).

- Liquidity Risk — Extreme market stress could temporarily hinder selling (though rare; post-2008 reforms strengthened MMFs).

Mitigation tactics include: laddering maturities, diversifying across issuers and instrument types, using only high-quality MMFs with liquidity gates, and monitoring credit ratings daily. Professional treasury software and conservative allocation policies keep risks minimal for most businesses.

28,237 Professional Market Research Stock Photos – Free & Royalty-Free Stock Photos from Dreamstime

Business Money Market vs. Capital Market

It is crucial to distinguish the two:

Business Money Market

- Short-term (≤1 year)

- Focus: Liquidity & safety

- Instruments: T-bills, CP, CDs, repos, MMFs

- Lower risk, lower return

- Used for working capital & cash management

Capital Market

- long-term (>1 year)

- Focus: Growth & capital formation

- Instruments: Stocks, corporate bonds, long-term loans

- Higher risk, higher potential return

- Used for expansion, acquisitions, and infrastructure

Businesses use the business money market for daily operations and the capital market for strategic growth. Understanding this distinction prevents mismatched financing decisions.

A history of trading floor design | Technology Desking™

Current Trends and Outlook for Business Money Market in 2026

The business money market stands at an inflection point in 2026. Despite falling interest rates, institutional money market assets have hit record highs of approximately $8 trillion globally. Liquidity remains abundant, driven by healthy corporate balance sheets and front-loaded fiscal stimulus in major economies.

Key 2026 trends shaping the business money market:

• Tokenization & Digital Innovation — Blockchain-enabled tokenized money market instruments are gaining traction, promising faster settlement and 24/7 access.

• AI-Powered Management — Treasury platforms now use artificial intelligence for predictive cash forecasting and automated yield optimization.

• Intensifying Competition — Portals and fintech platforms are driving down fees and improving transparency for corporate investors.

• Resilient Global Growth — Economists forecast sturdy 2.8% global GDP growth, supporting corporate cash flows and MMF inflows. Nearly 73% of business leaders expect revenue increases, creating more surplus cash for the business money market.

• Rate Environment — Moderating policy rates are reducing yields slightly, yet MMFs continue to offer attractive risk-adjusted returns compared with bank deposits.

Investment outlooks also highlight broadening opportunities, with private equity and direct lending complementing traditional money market strategies for sophisticated treasury teams. Overall, 2026 looks positive for businesses leveraging the business money market intelligently.

How Businesses Can Participate in the Money Market

Getting started is straightforward:

- Open a corporate brokerage or money market account with a reputable bank or platform.

- Work with treasury advisors to assess cash-flow patterns.

- Diversify across 3–5 instruments matching your liquidity needs.

- Use technology for real-time monitoring.

- Review policies quarterly to adapt to rate changes.

Even small businesses can access institutional-quality options through sweep accounts or low-minimum MMFs.

Conclusion

The business money market isn’t only a niche financial product—it’s an adaptable, powerful engine that fuels day-to-day operations, secures capital, and creates reliable income streams for companies worldwide. By gaining a command of its instruments, learn its advantages and pitfalls, and keeping an eye on 2026 developments such as tokenization and AI integration, companies can generate money that might otherwise lie dormant into a competitively useful stream.

Before you do, remember that whether you are optimizing treasury operations in Dhaka or balancing global growth, the business money market has robust tools for resilience and scalability. Begin assessing your cash management strategy today—your balance sheet will thank you tomorrow.