Introduction: What Are Credit Cards?

Credit cards are like magic plastic cards that let you buy things without using cash right away. In the United States, millions of people use them every day. They are important in modern finance because they help people manage money, build trust with banks, and even get rewards. Imagine going to a store and swiping a card to get what you want. That’s a credit card!

Credit cards allow you to borrow money from a bank or other company. You plan on paying it back later. The bank treats the store on your behalf, and then you settle up with the bank. It’s like a short loan. You should know them as a beginner because they can be good (or bad) for your money life. If you use them properly, you can establish a positive credit history.

This history is a kind of report card that determines whether you’re good with money. When you apply for a loan—to buy a car or house, for instance—banks check it. But failing to pay back the same can lead to issues like added fees or a bad mark.

In the United States, credit cards are ubiquitous. You find them at gas stations, online shops, and restaurants. They simplify life, but you must know the rules. This guide is intended for credit card novices like you in the United States. We’ll discuss how they work and the pros and cons. You’ll know whether one is right for you by the end.

Think of a credit card as a tool, not a toy. It can help you in emergencies, like when your bike breaks and you need parts. But always remember, it’s borrowed money. You have to give it back. Many kids in class eight might see their parents use them. Now, you can learn too. Credit cards started long ago, but now they’re super common. In 2026, almost everyone has one. But starting right is key.

How Do Credit Cards Work?

Credit cards are simple once you know the basics. First, there’s a credit limit. That’s the most money you can borrow. Like, if your limit is $500, you can’t spend more than that. The balance is what you owe. If you buy a toy for $20, your balance is $20.

Interest rates are important. They’re that little bit of extra money you give over if you don’t repay on time. We call it APR, or Annual Percentage Rate. If the APR is 20%, you pay an additional 20% on what you owe every year. But if you pay off in full each month, no interest!

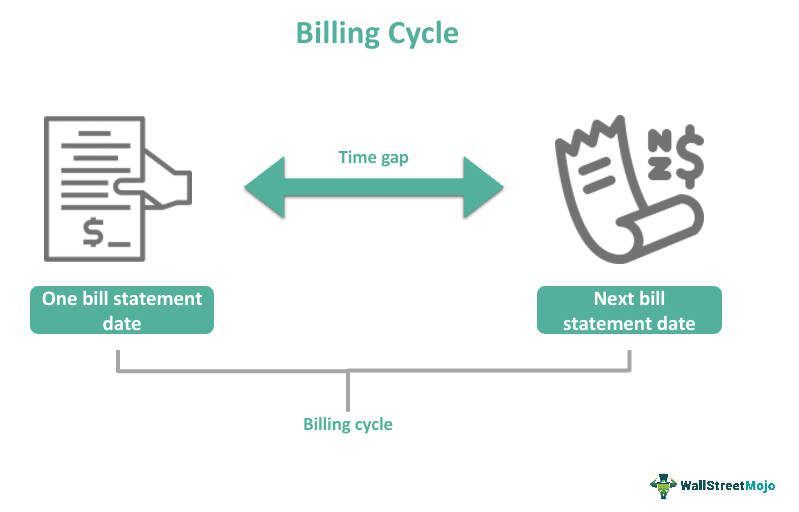

Repayment means reimbursing borrowed money. You get a bill each month. Or, pay at least the minimum—it’s even better to pay all. Your billing cycle is the period of time between the due dates for your bills, usually 30 days. All the while, you spend, and at the end of this period, you receive a statement detailing what you purchased.

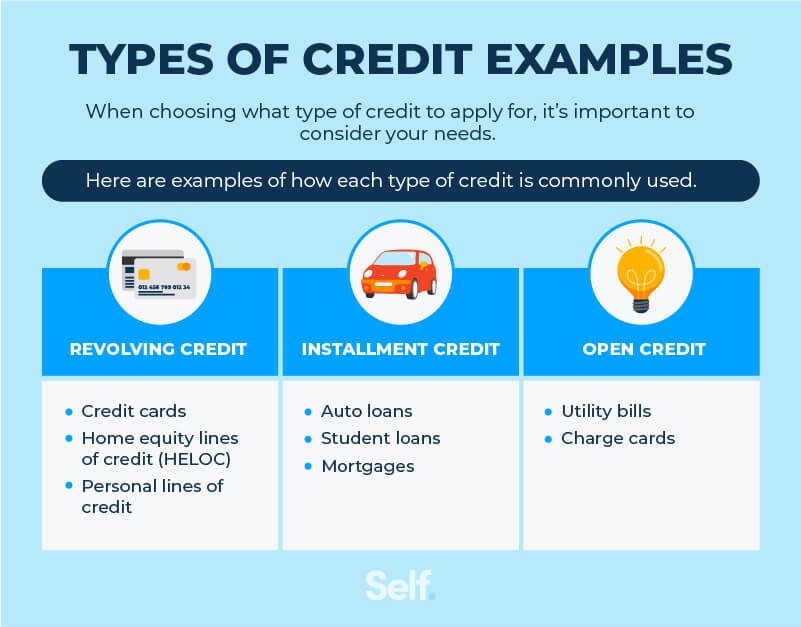

Revolving credit means you can borrow as you pay back. Pay down $100, and you can spend another $100. It’s like a circle. Most cards in the US are like these.

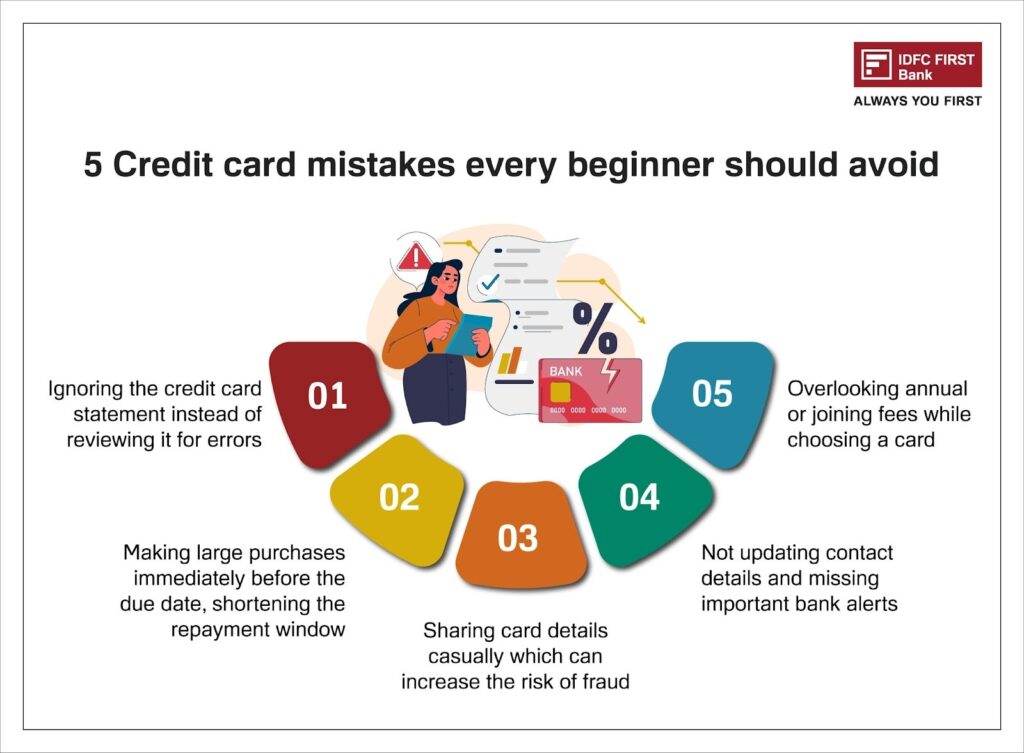

For example, you purchase lunch for $10. The store is paid by the card company. You pay the company later. If you pay on time, great! If not, interest adds up. #4 Always verify for mistakes in your statement.

Billing Cycle Definition—What Is It, How To Know, Example

Understanding this helps beginners. Don’t spend more than you can pay. Track your buys. Apps can help. In class eight, think of it like borrowing a pencil. You use it, then give it back. If you don’t, you might owe more. Credit cards teach responsibility.

Types of Credit Cards

There are many kinds of credit cards. Each is for different needs. Rewards cards give points or miles for spending. Use them for shopping, and get free stuff later.

Cashback cards give money back. Spend $100 on groceries, get $2 back. Good for everyday buys.

Travel cards are for trips. They give miles for flights or hotel points. Some have no foreign fees.

Student cards are for young people in school. They have low limits and help build credit. Easy to get if you’re a student.

Secured credit cards need a deposit. Give $200 to the bank, get a $200 limit. Good for beginners with no credit history.

For beginners, pros and cons: Rewards cards pros: free things. Cons: might spend more to get rewards. Cashback pros—save money. Con: annual fees sometimes. Travel pros—trip perks. Cons: high APR if not paid. Student pros – easy approval. Cons: low limits. Secured pros – builds credit. Cons: need a deposit.

Choose based on what you do. If you shop a lot, cashback. If traveling, a travel card.

The 3 Main Types of Credit Explained – Self. Credit Builder.

In the US, big companies like Visa and Mastercard offer these. Beginners start with secured or student. They help learn without big risks. Think of picking a game. Each has its own rules. Pick what fits you.

Key Features to Consider When Choosing a Credit Card

Pay attention to interest rates when choosing a credit card. APR is key. Low APR means less additional payment if you carry a balance.

Fees matter. The annual fee is the yearly cost of having this card. Some are $0, some $100. Dean said he knows the fines if you pay late, like $30. Choose no-fee for beginners.

Rewards programs give bonuses. Points for gas or food. Compare them to your spending.

Read the terms and conditions. It’s the rules. Grace period—time to pay without interest

To compare, use websites. Look at APR, fees, and rewards. Make a list. Card A: No intro APR for 50; $0 bonus. Card B: 2% cashback, $20 fee.

For beginners, pick simple ones. No annual fee, low APR.

Think about shopping for shoes. Check size, color, and price. Credit cards are the same. Ask parents or use online tools. In the US, laws protect you, like no surprise fees.

Benefits of Using a Credit Card

Credit cards have good sides. They build a credit score. Pay on time, and the score goes up. A good score helps get loans later.

Financial flexibility—buy now, pay later. Emergency? Use the card.

Earn rewards like cash or points. Buy groceries, get money back.

Protection: Fraud protection. If stolen, you don’t lose money. Purchase protection—if the item breaks, get a refund.

In the US, laws make cards safe. Zero liability for fraud.

Website Design Benefits Using Credit Card Stock Vector (Royalty Free) 1659982087 | Shutterstock

Like a shield. Also, track spending easily with statements. Beginners learn money habits. Rewards are fun, like game points.

Risks and Drawbacks of Credit Cards

But watch out. High interest rates if not paid. Debt piles up.

Debt accumulation—spend too much, owe lots.

Negative on credit score due to late payments.

Avoid mistakes: Don’t max out a card. Keep usage under 30%. No cash advances—high fees.

Tips: Budget, pay in full each month.

First Credit Card Guide for Beginners: Smart Tips to Start Right

Like eating candy. Too much bad. Use wisely.

How to Build and Maintain Good Credit with a Credit Card

Use responsibly. Pay on time always.

Credit utilization ratio—Use less than 30% of the limit.

Timely payments are 35% of the score.

Best practices: Set reminders, auto-pay.

Improve score by small uses, full pays.

Like building blocks. Each good pay adds up.

Understanding Credit Card Fees

Common fees: Annual – yearly. Late payment—if late. Foreign transaction—abroad buys. Cash advance—get cash.

Minimize: Pick no-fee cards, pay on time, and avoid advances.

Know them to save.

How to Avoid Credit Card Debt

Tips: Budget and track spending. Pay the full balance monthly.

No interest if paid in full.

Manage payments: Set alerts.

8 Proven Steps to Quickly Get Out of Debt and Save Money

Conclusion: Is a Credit Card Right for You?

Recap: Credit cards borrow money and have types, benefits, and risks.

For beginners, if responsible, yes. Use wisely.

Understanding Credit Cards: Key Concepts and Benefits for You | Nectar Money

Think if you can pay back. If yes, good tool.